The Invisible Risk: Why Financial Silence Often Triggers a Credit Score Decline

We often treat credit like a trophy on a shelf, something that stays polished as long as we do not drop it. But credit is more like a muscle; if you stop lifting, it starts to atrophy, and that is where it gets tricky for the disciplined saver. The algorithms managed by Equifax, Experian, and TransUnion are ravenous for fresh data, specifically "recent" activity that proves you still know how to handle a revolving balance without spiraling into a crisis. But when you stop swiping, the stream of data dries up. This leads to a state of being "unscorable" or having a "thin file," which is basically a financial vacuum that lenders find terrifying. Credit scores require active participation to maintain their structural integrity, yet most people think of it as a permanent grade from a high school test they took years ago. We are far from it.

The Scoring Models Demand a Pulse

Think about FICO 8, the workhorse of the industry. It looks at your last six months of activity to generate a reliable number. If you haven't touched a card in three years, the model might not even find enough evidence to give you a score at all. Is that fair? I think it is an absurd way to measure reliability, yet that is the game we are forced to play. Because lenders operate on the principle of predictive behavior, a lack of data is viewed as a wild card, which is the one thing a bank hates more than a late payment. They would rather see you owe $50 on a $5,000 limit than see a $0 balance for forty consecutive months.

Understanding the Inactivity Trap

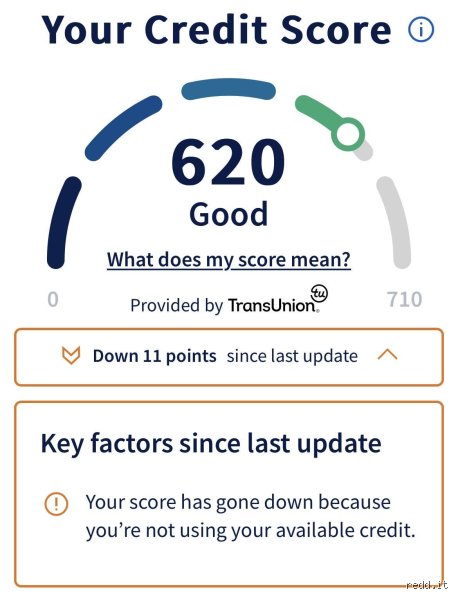

There is a specific phenomenon where an issuer—let’s say Chase or Amex—decides you are no longer profitable because you haven't generated a single cent in interchange fees or interest in two years. They close the account. Suddenly, your total available credit drops by, say, $10,000, and your credit utilization ratio spikes if you have balances elsewhere. That changes everything. One day you’re a 780, and the next, you’re sitting at a 720 because your "available headroom" evaporated while you were sleeping. It’s a ruthless efficiency move by banks to reclaim credit lines from dormant users and give them to someone who will actually spend.

The Mechanical Failure: Breaking Down the Loss of Credit Utilization and History

When we talk about the mechanics of a plummeting score due to neglect, the heaviest hitter is the utilization rate, which accounts for roughly 30% of your total FICO calculation. If you have three cards with $5,000 limits each, your total potential "spend power" is $15,000. Use $1,500 of that, and you are at a healthy 10% utilization. But if two of those cards get shuttered for inactivity, your total limit collapses to $5,000. Now, that same $1,500 balance represents a 30% utilization rate—a threshold that usually triggers a downward trend in your score. The issue remains that you didn't change your spending habits at all; the "bucket" simply got smaller around you. It’s like being penalized for the size of the glass rather than the amount of water inside.

The Erasure of Account Longevity

And then there is the "Age of Credit" factor, which contributes 15% to your score. People don't think about this enough when they decide to stop using their oldest card from college. If that 15-year-old account gets canceled by the creditor because you haven't used it for a pack of gum since 2021, your average age of accounts (AAoA) takes a massive hit once that closed account eventually falls off your report. It doesn't happen instantly—closed accounts in good standing stay on your report for ten years—but the loss of the "open" status can influence how some newer models perceive your current stability. Why would you let a decade of perfect history vanish just because you couldn't be bothered to buy a coffee once a year?

The Disappearing Act of Credit Mix

Lenders love a "well-rounded" person, or at least the appearance of one. This means having a mix of revolving credit (cards) and installment loans (cars, mortgages). If you pay off your only car loan and then stop using your credit cards, you essentially stop reporting any diverse financial behavior. As a result: your file goes stagnant. Experts disagree on how much this "silence" hurts in the short term, but honestly, it's unclear how many months of zero activity it takes for a specific score to start dipping. Some see a drop after four months of inactivity, while others coast for a year before the algorithm notices the lack of heartbeat.

The Math of Dormancy: Comparing Active Users to Debt-Free Ghosts

Let's look at a concrete example from a 2024 analysis of consumer behavior. Consider "User A," who has a $20,000 limit and spends $200 monthly, paying it off immediately. Contrast this with "User B," who has the same limit but hasn't touched a card in 24 months. User A consistently reports a 1% utilization. User B reports 0%. You might think 0% is better, right? Wrong. In many scoring tiers, 1% utilization outperforms 0% because it demonstrates the active, successful management of an open line. It is the difference between a pilot who flies every week and one who hasn't been in a cockpit since the Bush administration. Who would you trust more with your money? Hence, the "zero-balance penalty" is a very real, albeit small, drag on your potential peak score.

The Issuer’s Perspective on Maintenance

Banks are not charities; they are businesses that manage risk and capital. Every open credit line represents a "cost" to the bank in terms of capital they must keep in reserve. If you aren't using that $15,000 limit on your Capital One Venture or Citi Double Cash card, that is $15,000 of liability they are carrying for a customer who isn't making them any money. Which explains why they are so quick to prune the hedges. In 2023, several major issuers lowered the threshold for "inactivity closures" to as little as 12 months. If you lose an account that was opened in 2012, the sudden contraction of your credit history depth is a self-inflicted wound that takes years to heal.

Nuance in the Zero-Balance Strategy

But we have to be careful here because there is a counter-argument to the "always use it" mantra. For those with a history of compulsive spending, the risk of "losing a few points" due to inactivity is far lower than the risk of spiraling into 24.99% APR interest. I would argue that a slightly lower credit score is a fair price to pay for total mental peace and a debt-free life. Yet, for someone trying to buy a house in Denver or Seattle in two years, that 20-point drop caused by an automated account closure could be the difference between a 6.5% and a 7.2% mortgage rate. In short, the cost of being a "credit ghost" is often hidden until the moment you actually need to borrow money again.

The Hidden Velocity of Credit Reporting

The system is designed for movement. Every month, your creditors send a "snapshot" of your balance to the bureaus. When that snapshot consistently reads $0, the information being fed into the machine is essentially "null." It’s not "good" or "bad"; it’s just empty. But the machine is designed to reward positive proof of repayment. When you don't use the card, you aren't repaying anything, so you aren't earning the "on-time payment" checkmark for that month in the same way an active user is. Over time, your report looks less like a map of a thriving city and more like a ghost town. And who wants to invest in a ghost town? Because the lack of recent payment history can eventually lead to a "stale" report, you are effectively opting out of the very system that determines your financial mobility.

The Graveyard of Plastic: Common Blunders and Credit Score Myths

Many consumers operate under the misguided impression that a dormant credit card is a neutral asset, a silent guardian sitting in a drawer. The problem is that credit bureaus crave activity to measure your reliability. When you stop swiping, the data stream dries up. One pervasive myth suggests that closing an unused account protects your rating from theft or mismanagement. In reality, terminating an old account instantly truncates your credit history length and spikes your utilization ratio. If you have a total limit of $10,000 and close a $3,000 card you never use, your remaining debt is suddenly measured against a much smaller pool. Because the algorithm views this as a reduction in your available safety net, your score might take a sudden, painful dive.

The "Set It and Forget It" Trap

Losing track of recurring subscriptions is another classic pitfall. You might think your credit score won't fluctuate if the card remains at a zero balance, yet a forgotten $10 annual membership fee can trigger a delinquency notice if the statement isn't monitored. Small, ignored balances are the silent killers of high ratings. Let's be clear: a single payment missed by thirty days can slash a 780 score by up to 100 points. You are not being "safe" by ignoring the card; you are simply being blind to potential errors. And who wants to lose a decade of perfect history over a mismanaged streaming service fee?

Misinterpreting the "Zero Balance" Strategy

While keeping debt low is wise, maintaining a literal $0 balance across every single account can backfire. FICO models sometimes struggle to calculate a risk profile for someone who appears to have no credit usage whatsoever. Does credit score go down if you don't use it? Not immediately, but the lack of active reporting makes you a ghost to lenders. Statistics from major bureaus indicate that borrowers with a 1% to 6% utilization rate often see higher scores than those with 0% across the board. The issue remains that lenders want to see that you can handle debt, not just avoid it like a plague.

The Inactivity Execution: Why Banks Pull the Plug

Banks are not charitable organizations; they are businesses looking for a return on their capital. If your card gathers dust for twelve to twenty-four months, the issuer might unilaterally decide to shutter the account. They would rather allocate that credit line to a customer who generates transaction fees. This "inactivity closure" is a stealthy destroyer of credit health. You wake up one morning to find your available credit has vanished, which explains why your debt-to-income ratio looks suddenly bloated. To prevent this, experts suggest the "subscription method": link a small, monthly $15 charge to the card and set up an automatic full payment from your checking account.

The Data Decay Factor

Credit scoring is a game of predictive analytics based on recent behavior. When an account goes dark, the weight of that positive history begins to erode in favor of newer, perhaps less favorable, data points. It is like an athlete who stops training; the past trophies still exist, but the current performance is what scouts care about. You must feed the machine. A simple $5 grocery purchase every six months is usually enough to keep the reporting status "active" and ensure the bank keeps the line open. (Yes, even a pack of gum serves the purpose of maintaining your financial pulse).

Frequently Asked Questions

How long does it take for inactivity to impact my credit file?

Most lenders report to the three major bureaus every thirty days, but they typically wait between six and eighteen months of total silence before considering an account "inactive" or moving toward closure. Data suggests that account longevity accounts for 15% of your total score, so losing a ten-year-old card due to neglect is a significant setback. If the bank closes the account, the history may stay on your report for ten years, but its positive impact on your utilization ratio vanishes instantly. As a result: you could see an immediate drop of 20 to 50 points depending on your other available limits.

Does credit score go down if you don't use it for small daily purchases?

Your score does not care if you are buying a yacht or a soda, provided the activity is reported. The algorithm focuses on the statement balance relative to the credit limit, not the volume of transactions you process monthly. You can maintain a pristine rating by using the card only once or twice a year, as long as the account remains open and in good standing. Yet, the risk of a bank-initiated closure is higher if you only use it annually, making quarterly usage a much safer bet for long-term stability.

Will my score recover quickly if I start using an old card again?

Recovery is usually swift because the utilization math recalibrates as soon as the next billing cycle is reported to the bureaus. If your score dropped because an account was closed for inactivity, the damage is more permanent since you cannot easily "un-close" a card without a new hard inquiry. Re-establishing activity on a dormant but still open card can provide a modest boost within thirty to sixty days as the "active" status is refreshed. In short, it is far easier to maintain a score through minimal effort than to rebuild one after a total collapse of your credit age.

The Verdict on Financial Ghosting

The hard truth is that modern finance demands your constant, albeit minimal, participation. Treating credit like a "break glass in case of emergency" tool is a fundamental misunderstanding of how lending ecosystems function. You cannot expect a high score if you refuse to provide the data necessary to calculate it. Our stance is firm: financial passivity is a risk you cannot afford in a world governed by algorithms. Stop fearing the plastic and start managing it with surgical precision. But don't expect the bureaus to reward your silence with anything other than a slow, steady decline into credit irrelevance. Manage your tools, or they will eventually be taken away from you.