The Mirage of the Midas Touch: Understanding the Trump Business Philosophy

To grasp why so many Donald Trump's failed businesses exist, you first have to unlearn everything you know about traditional risk management because the man operates on a different frequency entirely. Most CEOs view a bankruptcy as a scarlet letter—a stain on the soul of their professional reputation—yet for the Trump Organization, it functioned more like a strategic escape hatch or a financial reset button. And that changes everything when you try to analyze his track record. It wasn't always about the product being bad; sometimes the math was simply rigged against the reality of the market from day one.

The Psychology of the Pivot

Where it gets tricky is the gap between the gold-plated name on the building and the actual liquidity behind the scenes. Trump’s strategy frequently involved leveraging his personal brand to secure massive loans, effectively making the "Trump" name the primary collateral for projects that were often over-leveraged and under-researched. Because he convinced lenders that his involvement was indispensable for success, banks kept feeding the machine even as the red ink began to flow. People don't think about this enough: he wasn't just selling real estate; he was selling the invincible perception of wealth, which meant that even when a company died, the brand usually survived the autopsy.

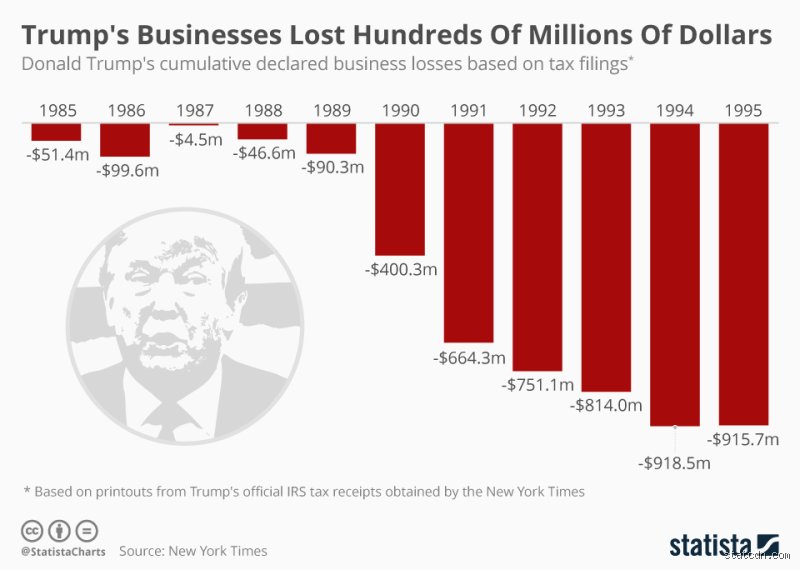

The Debt Trap and the 1990s Reckoning

But the bill always comes due, doesn't it? By the early 1990s, the aggressive expansion into Atlantic City and the acquisition of the Plaza Hotel had created a debt load so massive—roughly $3.4 billion in total corporate debt—that even the most optimistic projections couldn't keep the lights on. This era birthed the most famous of Donald Trump's failed businesses, proving that even a massive ego cannot stop the cold mechanics of interest rates. Experts disagree on whether he was a victim of a cooling economy or his own hubris, but honestly, it's unclear if he ever intended to pay those original terms back anyway.

High Stakes and Dead Ends: The Atlantic City Casino Meltdowns

The crown jewels of the Trump empire were supposed to be the boardwalk palaces, but they eventually became the most expensive lessons in commercial insolvency in New Jersey history. We're far from it being a simple case of "the house always wins" when the house is carrying more debt than it can possibly generate in blackjack revenue. Between 1991 and 2009, his casino properties filed for bankruptcy four times. This wasn't just a streak of bad luck; it was a systemic failure of a business model that prioritized glitz over the boring, necessary work of balance sheet maintenance.

The Taj Mahal: A "Eighth Wonder" in Chapter 11

When the Trump Taj Mahal opened in 1990, it was the largest and most expensive casino in the world, costing $1.1 billion to construct and decorate with Austrian crystal chandeliers. Yet, less than a year after the ribbon-cutting ceremony, the "Eighth Wonder of the World" defaulted on its interest payments because it needed to pull in an impossible $1.3 million a day just to break even. It is the ultimate example of a project being "too big to fail" while simultaneously being too bloated to fly. As a result: the casino entered bankruptcy in 1991, with Trump ceding 50 percent ownership to bondholders in exchange for lower interest rates and more time. But did he really lose? While the business suffered, he stayed in the game, a recurring theme in the saga of Donald Trump's failed businesses.

Trump Plaza and the Castle: Cannibalizing the Empire

The issue remains that Trump wasn't just competing with Steve Wynn or Merv Griffin; he was effectively competing with himself. By owning three massive casinos in the same small geographic footprint, he cannibalized his own customer base, leading to the 1992 bankruptcy of the Trump Plaza Hotel and the Trump Castle. Think about the sheer logistical madness of trying to keep three massive gambling floors full in a city that was already starting to feel the squeeze of regional competition. It was like trying to run three different bakeries on the same block and wondering why you're throwing away half the bread at the end of the night.

The Boutique Failures: When Brand Extension Goes Wrong

Beyond the heavy machinery of the casino industry, the list of Donald Trump's failed businesses includes a graveyard of consumer products that were meant to make the billionaire lifestyle accessible to the average Joe. These weren't just side projects; they were attempts to turn a last name into a lifestyle ecosystem. Except that the public wasn't always buying what he was selling, leading to a series of quiet exits and loud lawsuits.

Trump Steaks and the Sharper Image Blunder

Perhaps no failure is as frequently mocked as Trump Steaks, which launched in 2007 with a campaign that featured the future president standing next to a platter of meat like a high-end butcher. Sold exclusively through The Sharper Image—a store better known for ionic breeze air purifiers and massage chairs—the steaks were priced between $199 and $999. It was a bizarre retail marriage that lasted only two months before being pulled from the shelves. Why would anyone buy a filet mignon from the same place they buy a robotic vacuum? Which explains why the product vanished so quickly: it was a total mismatch of brand identity and consumer behavior.

Trump Airlines: Flying Too Close to the Sun

In 1989, Trump spent $365 million to buy the Eastern Air Shuttle, a reliable, no-frills service for business travelers between New York, Boston, and D.C. He added gold-plated bathroom fixtures, faux-marble floors, and thick carpeting—features that added weight and cost but didn't necessarily appeal to people who just wanted to get to their 9:00 AM meeting on time. The timing was disastrous, coinciding with a spike in jet fuel prices and the start of a recession. Within three years, the airline was handed over to creditors. It turns out that luxury in the sky is a hard sell when the ground beneath your feet is shifting.

A Comparative Look: How Trump's Failures Stack Up Against Peers

If we look at other real estate moguls of the era, the frequency of Donald Trump's failed businesses stands out as an anomaly of high-volume volatility. Most developers of his stature, like the Durst or Ross families, tend to hold onto assets for generations, favoring stability over the flashy, high-leverage gambles that Trump preferred. Yet, those families also don't have the same cultural footprint. Trump’s willingness to fail publicly and often is, paradoxically, what kept him in the headlines and, eventually, in the White House.

The Real Estate Cycle vs. The Trump Cycle

The standard real estate cycle is dictated by interest rates and supply, but the "Trump Cycle" was dictated by the velocity of fame. While a traditional firm might go under and disappear, a Trump failure was usually followed by a new licensing deal or a reality TV contract. In short: he figured out how to monetize the fallout. This distinguishes him from a peer like Sam Zell, who focused on "distressed assets" with surgical precision. Trump wasn't looking for value in the ruins; he was looking for the next spotlight, even if the stage was built on a foundation of debt. This brings us to a uncomfortable truth about modern business—sometimes being famous is more valuable than being profitable.

Common Pitfalls in Evaluating Donald Trump's Failed Businesses

The problem is that the public often views corporate liquidation through a lens of personal failure rather than calculating strategic maneuver. When we examine Donald Trump's failed businesses, we must differentiate between an operational collapse and a tactical retreat. Many critics assume every bankruptcy filing equals a total loss of net worth. This is a mirage. In reality, the Chapter 11 process allowed the Trump Organization to shed debt while retaining management fees. Because of this, the "failure" often fell squarely on the shoulders of bondholders and contractors rather than the namesake himself. It was a divestment of risk that protected the core brand while the peripheral entities burned. Let's be clear: the house did not always lose, even when the casino did.

The Branding Versus Equity Delusion

One massive misconception involves the actual ownership structure of late-era projects. You might see the gold letters and assume a direct equity stake. Except that many of these ventures were merely licensing agreements where Trump provided the name for a fee. When Trump Ocean Resort Baja or Trump Tower Tampa cratered during the 2008 housing crisis, he was often a paid spokesperson rather than the developer. The issue remains that the public conflates intellectual property licensing with capital-intensive development. This distinction is vital. It transformed the risk profile of his portfolio from a traditional real estate mogul to a high-margin marketing machine. And yet, the fallout for the actual investors in these ghost towers was devastatingly tangible.

The Bankruptcy Math Mystery

Why did the casinos fail while the man stayed on the Forbes list? The math is counterintuitive. Between 1991 and 2009, his Atlantic City properties entered bankruptcy six times. As a result: institutional lenders were forced to take haircuts on billions of dollars in debt. But during the 1991 Taj Mahal restructuring, Trump gave up half his stake in exchange for better terms and a lower interest rate. (A classic move for someone who treats debt like a suggestion rather than a mandate). We often confuse a company's balance sheet with an individual's wallet. They are not the same thing. In short, the Trump Hotels & Casino Resorts entity was a public vehicle that absorbed the shocks of the 1990s gambling slump while the private Trump assets remained insulated behind a wall of corporate personhood.

The Expert View: The Pivot to Reality Television as a Lifeline

If you want to understand the true trajectory of Donald Trump's business career, you have to look at the early 2000s. The Atlantic City era had left a trail of high-yield debt and skeptical banks. Major Wall Street firms were no longer eager to lend. Then came Mark Burnett. The success of The Apprentice was not just a media win; it was a total recalibration of his business model. It shifted the revenue stream from volatile brick-and-mortar hospitality to the guaranteed cash flow of "royalty-style" income. Which explains why he could walk away from failing ventures like Trump Steaks or GoTrump.com without sweating. He wasn't selling products. He was selling a mythology of competence.

The Ghost of Trump Mortgage

The timing of Trump Mortgage in 2006 is perhaps the most glaring example of a missed market signal. Despite the looming subprime shadow, the company launched with claims that it would become the top lender in the nation. It lasted roughly 18 months. The issue remains that the venture relied on market momentum rather than actual industry innovation. It proved that even a powerful brand cannot override the gravity of a collapsing macro-economic cycle. This failure highlights a recurring theme: an over-leveraged reliance on the assumption that the "Trump" name could insulate a business from the cold reality of supply and demand.

Frequently Asked Questions

What were the actual losses in the Atlantic City casino bankruptcies?

The cumulative debt restructured during the various Atlantic City filings exceeded $4.7 billion across two decades. In the 1991 Taj Mahal filing alone, the property carried nearly $1 billion in high-interest junk bonds. While the corporate entities faced massive write-downs, Trump himself often negotiated deals that allowed him to remain as a figurehead or manager. This strategy ensured that while public shareholders and bondholders lost significant value, the branding value of the properties remained intact for future licensing. The 2004 filing of Trump Hotels & Casino Resorts saw a further reduction of his ownership stake from 47 percent to roughly 27 percent to satisfy creditors.

Did Trump Steaks and Trump Vodka fail because of the product quality?

The demise of these consumer goods had less to do with the liquid in the bottle and more to do with distribution friction and brand misalignment. Trump Steaks launched in 2007 exclusively through Sharper Image and QVC, a bizarre choice for a luxury food item. Sales were reportedly lower than $1 million for the entire run. Trump Vodka suffered from a similar lack of market penetration, eventually losing its trademark protection in certain regions due to non-use. These were low-overhead experiments that failed to gain the retail velocity required to compete with established giants like Grey Goose or Omaha Steaks.

How many times has Donald Trump personally declared bankruptcy?

The answer is zero, despite the common internet meme suggesting otherwise. There is a profound legal distinction between personal bankruptcy and the Chapter 11 restructuring of a business entity. All six filings—including the Plaza Hotel in 1992 and the various iterations of the Trump Entertainment Resorts—were corporate reorganizations. This allowed him to keep his personal homes, planes, and private assets while the legal entities took the financial hit. It is a sophisticated use of the American legal system that prioritizes corporate continuity over creditor satisfaction. But was it an ethical use of the law or merely a clever one?

A Final Perspective on the Legacy of Failure

Evaluating Donald Trump's failed businesses requires us to abandon the binary of "win or lose" and look at the velocity of capital. We cannot simply tally the shuttered storefronts and declare the man a fraud, nor can we ignore the mountain of unpaid vendors left in the wake of the 1990s. The truth is that his greatest business achievement was the commodification of his own reputation, which turned even his bankruptcies into a form of perverse marketing. He transformed the American bankruptcy code into a tool for personal wealth preservation. This is the ultimate lesson for any observer: in the world of high-stakes real estate, a failure is only a failure if you didn't get paid to walk away. We see a graveyard of logos, but he sees a portfolio of tax write-offs and hard-learned leverage. Whether this is brilliant strategy or a systemic exploit is a question of your own economic values.