Understanding the Genesis and the Weight of the Three Golden Rules

People don't think about this enough, but the double-entry system we use today was essentially perfected by a Franciscan friar named Luca Pacioli in 1494. Imagine a world where merchants in Venice were trying to track spice shipments across the Mediterranean without a standardized way to prove their math. It was a mess. Pacioli didn't just invent a math trick; he created a social contract for trust. But when we talk about the modern golden rule of accounting, we are actually looking at a triad of mandates that govern how Real, Personal, and Nominal accounts behave under pressure. This is where it gets tricky for the uninitiated.

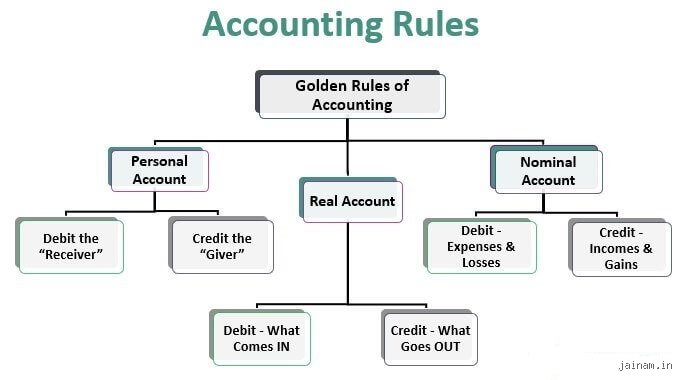

The Real Account Mandate: Tangible Truths

Debit what comes in, credit what goes out. That sounds simple, right? If your company buys a fleet of electric delivery vans in London for 500,000 GBP, that asset "comes in" to your books. You debit the Asset account. But because money isn't free—a harsh reality we all face—you must credit the Cash or Bank account because that value is "going out." I find it fascinating that even in an era of digital currencies and algorithmic trading, this physical logic of "in and out" remains the safest harbor for auditors. If a CFO tries to tell you otherwise, they are likely selling a fantasy that will eventually collapse under the weight of an SEC investigation.

Deciphering the Personal and Nominal Account Logic

Moving away from physical assets like buildings or gold bars, we hit the Personal Accounts. These involve people, firms, or associations. The directive here is sharp: debit the receiver and credit the giver. If a vendor in Singapore provides you with raw materials on credit, they are the "giver" of value. You credit their account. Why does this matter? Because it tracks the legal obligation of debt. But wait, what about the abstract stuff? That is where Nominal accounts enter the fray. They handle the "ghosts" of the financial world—expenses, losses, incomes, and gains. The rule shifts again: debit all expenses and losses, and credit all incomes and gains. It is a mirrored universe where a "debit" to an expense account actually feels like a negative to your bank balance, yet it is a positive entry for the record-keeping of your operational costs.

The Friction Between Personal Obligations and Nominal Results

But here is the nuance that many textbooks gloss over: the tension between these accounts is what creates a Trial Balance that actually functions. If you pay a consultant 10,000 USD for a market strategy, you are dealing with a Nominal account (the expense) and a Personal or Real account (the cash). Which explains why a single error in categorization ripples through the entire General Ledger like a virus. Have you ever wondered why some multi-billion dollar corporations still report "unexplained variances"? It is usually because they lost track of the receiver/giver relationship in a complex web of subsidiary ledgers. In short, the golden rule of accounting acts as a self-correcting mechanism—at least in theory.

The Technical Architecture of the Accounting Equation

At the heart of every GAAP-compliant report is the 180-degree balance of the accounting equation: Assets = Liabilities + Equity. This is not just a suggestion; it is the law of the land. When we apply the golden rule of accounting, we are essentially performing a constant maintenance routine on this equation. In 2025, a study by the Financial Accounting Standards Board (FASB) noted that 92 percent of restatements in mid-cap firms were due to improper application of these very rules during high-frequency transactions. As a result: the complexity of modern business requires an even stricter adherence to these old-school principles than the Renaissance merchants ever needed.

The Debit-Credit Equilibrium in Complex Transactions

Let's look at a depreciation entry for a piece of manufacturing equipment in Germany valued at 1.2 million EUR. You aren't "paying" anyone when the machine gets older, so how does the rule apply? You debit the Depreciation Expense (Nominal) and credit Accumulated Depreciation (Real, or more specifically, a contra-asset). This keeps the balance. Honestly, it's unclear to some why we bother with such granular steps in the age of AI. However, the issue remains that AI models often hallucinate financial data if they aren't constrained by the rigid "left-side, right-side" architecture of the golden rules. We're far from it being obsolete; if anything, the immutable nature of a balanced entry is the only thing keeping digital finance from turning into a hall of mirrors.

Comparing the Golden Rules to Modern Alternatives

Some critics argue that Cash-Basis accounting is a simpler "rule" for the modern freelancer or the small corner shop in Brooklyn. In cash-basis, you just record when money hits the bank. No debits, no credits, no headache. Yet, this "alternative" fails the moment you need to scale or attract investors. Why? Because it ignores accruals. The golden rule of accounting, through the Accrual Basis, captures the economic reality of a transaction the moment it happens, regardless of when the cash moves. That changes everything for a business trying to project future growth. While cash-basis might tell you what you have today, the golden rules tell you what you are worth tomorrow.

The Fallacy of Single-Entry Systems

And let's be blunt: single-entry bookkeeping is a relic that should have stayed in the 19th century. It lacks the internal checks provided by the golden rule of accounting. Without the dual-effect of double-entry, you have no way to verify that your ending cash balance actually matches your total revenue minus expenses (unless you want to manually count every penny at the end of the night, which sounds like a nightmare). Experts disagree on many things—tax rates, valuation models, or the future of ESG reporting—but almost no one with a CPA designation disputes the necessity of the double-entry mandate. It is the one truth in a world of financial volatility.

Common pitfalls and the trap of the Golden Rule of accounting

The problem is that many neophyte bookkeepers treat the Golden Rule of accounting as a static mantra rather than a fluid logic gate. They often confuse the direction of flow. For instance, when a company receives a $5,000 cash injection from a loan, the novice might correctly debit Cash but fail to recognize the burgeoning Liability as the offsetting credit. Why does this happen? Usually, it is because they view "credit" through the lens of a personal bank statement where a credit feels like a win, whereas in double-entry bookkeeping, crediting a liability simply reflects where the value originated. It is a mirror world. You must unlearn your consumer habits to survive here.

The Revenue Recognition Mirage

Expectations collide with reality when service-based businesses record unearned revenue incorrectly. If a client pays you $12,000 upfront for a year-long consultancy, the Golden Rule of accounting dictates you debit Cash. However, you cannot credit Revenue yet. You must credit a Liability account. Yet, many firms prematurely inflate their profit margins by 15% to 25% by ignoring this distinction. This creates a ghost profit that vanishes upon audit. But is it really a profit if you still owe the work? No. (And your tax man will certainly agree with that assessment).

The "Contra-Account" Headache

Let's be clear: accumulated depreciation is the graveyard of many balance sheets. It is a contra-asset. It carries a credit balance while living in the asset section. This feels counter-intuitive. Because the Golden Rule of accounting requires every transaction to balance, people often try to force a debit where it does not belong. For a $40,000 delivery van, the annual depreciation might be $8,000. You debit the expense. You credit the contra-asset. If you mess this up, your Net Book Value becomes a work of fiction.

The Hidden Power of the Ledger: Expert Nuance

Beyond the basics lies the matching principle, which serves as the tactical heartbeat of the Golden Rule of accounting. Experts do not just move numbers; they time them. The issue remains that accrual accounting requires a level of psychic foresight that cash-based systems ignore. You are not just tracking money. You are tracking obligations and rights. When we look at a current ratio of 2:1, we are seeing the Golden Rule in a state of rest. It is the equilibrium of a firm's health. Which explains why veteran CFOs spend less time on the math and more time on the integrity of the source documents.

The Ghost in the Machine

The problem is the assumption that a balanced trial balance means the books are "right." It does not. You can debit the wrong asset or credit the wrong liability for $1,000,000 and the equation will still sit pretty at zero. Accuracy is not the same as balance. I argue that the Golden Rule of accounting is actually a diagnostic tool for internal fraud detection. When the math is perfect but the inventory turnover is lagging by 30%, someone is likely "cooking" the debit side. Balance is the minimum requirement, not the final goal. We must be more cynical about the numbers we see.

Frequently Asked Questions

Does the Golden Rule of accounting apply to small businesses?

Absolutely, because even a lemonade stand must distinguish between the $50 in the till and the $20 owed to the grocer for sugar. While 82% of small businesses fail due to cash flow mismanagement, those utilizing double-entry systems have a significantly higher survival rate over a five-year period. The rule provides a granular view of equity and debt that simple checkbook tracking ignores. As a result: you gain a professional-grade Balance Sheet that banks actually trust. Without it, you are just guessing at your net worth while the $10,000 you think you have slowly evaporates into overhead.

Can modern AI software replace the need to understand this rule?

Software is merely a fast way to make mistakes if you do not understand the underlying logic of debits and credits. While 90% of accounting tasks may soon be automated, the interpretation of anomalies remains a human burden. If an algorithm incorrectly categorizes a $15,000 capital expenditure as a routine repair, your EBITDA will be wrong. Automation handles the mechanical entry but fails at the conceptual alignment of the Golden Rule of accounting. You must remain the pilot of the machine.

What happens if a ledger does not follow the Golden Rule?

In short, the entire financial reporting structure collapses into a heap of unreconciled data. A discrepancy of even $0.01 indicates a systemic failure in the logic of the entry. In public companies, a failure to maintain these internal controls can lead to SEC fines or a plummeting stock price. Statistics show that financial restatements due to clerical errors can cost firms up to 10% of their market capitalization in a single day. The rule is the only thing standing between fiscal transparency and total corporate chaos.

A Final Word on Fiscal Symmetry

We must stop viewing the Golden Rule of accounting as a mere academic hurdle for first-year students. It is the universal law of conservation applied to the world of commerce. If you ignore it, your business is a house of cards waiting for a light breeze. I am convinced that the obsession with digital disruption has made us forget that the foundational math of the 15th century is still our best defense against bankruptcy. Balance is not just a preference; it is the moral center of every transaction. Do not just record your numbers. Respect the symmetry they demand, or prepare to watch your assets dissolve into thin air.