Understanding the Global Appetite: Why Pork Trade Is Getting Complicated

The thing is, nobody expected the global pork market to become this fragmented so quickly. We used to think of pig farming as a localized affair—farmers raising hogs for the nearest city—but those days are long gone. Today, a biological outbreak in a remote province of China can cause prices to skyrocket in a supermarket in Madrid within forty-eight hours. Because the supply chain is so tightly wound, the question of who ships the most meat becomes a barometer for national economic health. Global pork exports topped 10 million metric tons recently, a staggering figure that represents billions of dollars in "white meat" diplomacy. But why does one country win while another fails?

The Biological Factor: African Swine Fever and Market Shifts

You cannot talk about pig exports without mentioning the shadow of African Swine Fever (ASF). It decimated herds across Asia and parts of Eastern Europe, creating a vacuum that Western producers rushed to fill. When China’s domestic production cratered, the world changed. Suddenly, the Spanish white pig wasn't just a local delicacy; it became a strategic reserve for the East. Where it gets tricky is the biosecurity aspect, as countries like Germany—formerly a titan of the industry—found themselves locked out of lucrative markets because of a few wild boar carcasses found near their borders. It is a brutal, unforgiving game where a single virus strain can bankrupt an entire sector overnight.

The Spanish Hegemony: How a Mediterranean Powerhouse Took the Crown

Spain has pulled off what many thought was impossible: they modernized an ancestral industry into a high-tech export engine that now accounts for nearly 25% of all EU pork production. But it wasn't luck. The Spanish "Interporc" model integrated the entire process, from the genetics of the piglet to the final vacuum-sealed loin destined for a port in Guangzhou. And they did it while everyone else was distracted. While other nations were arguing over environmental regulations, Spanish producers were investing in cold-chain logistics and specific cuts tailored for the Japanese and South Korean markets. Have you ever wondered why your premium bacon might actually have traveled halfway around the world before hitting your frying pan?

The Integration Model and the "White Pig" Advantage

The secret sauce—if you will excuse the pun—is the vertical integration found in regions like Aragon and Catalonia. Large companies control every step of the life cycle. This reduces costs and, perhaps more importantly, ensures a level of traceability that nervous importers in Beijing demand. But it is not just about volume. They have successfully segmented their market, selling high-end Iberico products to connoisseurs while flooding the commodity market with standard white pork. The issue remains that this level of intensive farming puts a massive strain on local water resources, creating a tension between economic gain and environmental reality that the Spanish government is still trying to balance.

The American Contender: Efficiency, Corn, and Trade Wars

If Spain is the scalpel, the United States is the sledgehammer. The U.S. pork industry is built on a foundation of incredibly cheap feed, specifically the endless oceans of corn and soybeans grown in the Midwest. Because the cost of "finishing" a hog is largely the cost of what it eats, the U.S. has a natural competitive advantage that is hard to beat. In 2024, the U.S. exported roughly $8 billion worth of pork. Yet, the Americans are often at the mercy of Washington’s foreign policy. Trade disputes and tariffs can shut down a market like Mexico—which is the largest volume buyer of U.S. pork shoulder and hams—with the stroke of a pen. People don't think about this enough: a pig raised in Iowa is more a victim of trade policy than of actual market demand.

The Mexico Connection and the H-2A Labor Reality

Mexico is the heartbeat of the American export machine. They take the cuts that Americans don't want as much, like variety meats and bone-in hams, creating a perfect symbiotic relationship. However, the reliance on this single neighbor is a double-edged sword. If the USMCA agreement faces friction, the entire American pork belt feels the vibration. Furthermore, the industry is grappling with a massive labor shortage, relying heavily on foreign workers to staff the processing plants in places like South Dakota and North Carolina. It is an ironic twist—an industry that defines "Middle America" cannot function without a globalized workforce and international customers. That changes everything when you try to calculate the true "cost" of a pound of pork.

Brazil: The Rising Giant of the Southern Hemisphere

We're far from it being a two-horse race between the U.S. and Spain. Brazil has entered the chat with a vengeance. For a long time, Brazil was sidelined by foot-and-mouth disease concerns, but they have spent the last decade cleaning up their act and their herds. Now, they are the "wild card" of global protein. Because they have virtually unlimited land and are rapidly expanding their own grain production, their overhead is terrifyingly low for Western farmers. In recent years, Brazilian exports have surged by double digits, often filling the gaps when China gets into a spat with the West. It is a geopolitical pivot that has moved the center of gravity for the pork trade toward the Southern Hemisphere.

The Santa Catarina Fortress

Most of the action is centered in the state of Santa Catarina. Why? Because it was the first region in Brazil to be recognized as free of ASF and foot-and-mouth disease without vaccination by the World Organisation for Animal Health. This status is the "golden ticket" for exports. Brazilian producers like JBS and BRF—global titans you have likely heard of in the context of beef—are now applying that same industrial scale to swine. Honestly, it's unclear if the U.S. or the EU can compete with Brazil on price in the long run, especially as the Brazilians improve their infrastructure and port efficiency. They aren't just selling meat; they are selling a low-cost alternative to a world that is increasingly price-sensitive.

Myths and Miscalculations in the Porcine Trade

The Volume versus Value Trap

You probably think counting carcasses is the only way to crown a champion. It is not that simple. Many observers obsess over raw tonnage while ignoring the fiscal reality of high-value primal cuts versus processed offal. The problem is that a country might ship massive quantities of low-grade trimmings but lag behind in total revenue. Take Denmark, for example. They do not have the landmass of Brazil, yet their precision in exporting specialized genetics and premium bacon creates a disproportionate economic footprint. Numbers lie when you forget to check the price tag. Because of this, the leaderboard looks different depending on whether you value the weight of the pig or the weight of the wallet. Let's be clear: bragging rights for which country exports the most pork often shift based on seasonal demand for specific bellies or ribs rather than just sheer animal count.

The Transit Illusion

Have you ever considered how many pigs are actually just tourists? A massive misconception involves "re-exports" within the European Union. The Netherlands is a master of this logistical sleight of hand. They possess world-class ports like Rotterdam, which act as a global distribution hub for the entire continent. A shipment might arrive from Germany, sit in a warehouse, and then depart for Asia under a Dutch manifest. This inflates their statistics. As a result: the data often suggests a level of domestic production that simply does not exist on the ground. Which explains why tracking the origin of slaughter is far more accurate than tracking the port of exit. Relying on customs data alone is like judging a chef by the delivery driver who hands you the bag.

The Biosecurity Moat: An Expert Perspective

The African Swine Fever Barrier

The global trade map is currently being redrawn by a virus, not a trade deal. African Swine Fever (ASF) has devastated herds across Eurasia, turning former powerhouses into desperate importers overnight. Expert analysis suggests that biosecurity protocols are now the primary currency of the international market. If a nation cannot prove its borders are sterile, its export licenses evaporate. This is where the United States and Brazil have gained an aggressive foothold. They remain (for now) largely insulated from the outbreaks plaguing Europe and China. The issue remains that one stray ham sandwich at an airport could collapse a multi-billion dollar pork shipping industry in twenty-four hours. It is a fragile hegemony. We are witnessing a shift where "clean" status is worth more than low production costs.

Niche Dominance and Breed IP

Except that high-volume commodities are becoming a race to the bottom. I would argue the real winners are those dominating proprietary swine genetics and heirloom breeds. Spain has mastered this with the Iberico trade. They do not compete on price with the mega-farms of Iowa. Instead, they sell a story and a specific fat-marbling profile that commands four times the market average. But can every country replicate this luxury model? Probably not. It requires centuries of culinary branding. In short, the future of the top pork exporter title may belong to the nation that stops trying to feed the world cheaply and starts feeding the elite exclusively. My expertise has limits here; predicting consumer taste shifts is harder than predicting corn yields.

Frequently Asked Questions

Which nation currently holds the top spot for total pork export volume?

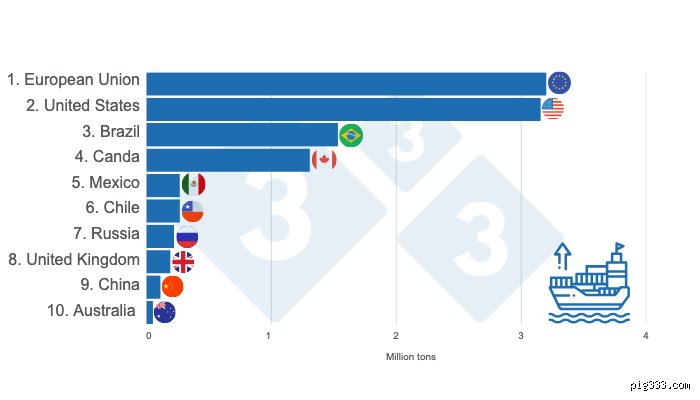

The European Union collectively dominates the landscape, but as a single entity, Spain has recently surged to the forefront of the global stage. In 2023, Spanish shipments exceeded 2.7 million metric tons, capitalizing on aggressive trade agreements with China. The United States follows closely, often trading places depending on the strength of the dollar and domestic hog slaughter rates. Brazil is the rapidly rising challenger, boasting a 15% increase in year-on-year exports to various Asian markets. These three players effectively control the flow of the world's most consumed protein.

How does China influence the rankings of pork exporting countries?

China is the sun around which the entire porcine solar system orbits. Although they are the world's largest producer, their domestic demand is so gargantuan that they remain a net importer. When their internal supply fluctuates due to disease or environmental regulations, they can single-handedly drive up the global pork price index. A slight 5% shift in Chinese demand can trigger a massive production spike in Brazil or Germany. This creates a volatile cycle where which country exports the most pork is often determined by who has the best political relationship with Beijing at that moment.

What role does the exchange rate play in swine trade dominance?

Currency fluctuations are the silent killers of export contracts. When the Euro is weak against the Dollar, Spanish and German ham becomes incredibly attractive to buyers in Tokyo or Mexico City. Conversely, a strong US Dollar can price American farmers out of competitive markets even if their operational efficiency is superior. Exporting is not just about farming; it is a complex game of foreign exchange hedging and geopolitical maneuvering. Buyers will often ignore quality differences of 5% if the currency swing offers a 10% discount on the final invoice.

The Final Verdict on Global Swine Supremacy

The era of stable, predictable protein flows is dead. We must stop viewing which country exports the most pork as a static trophy and start seeing it as a temporary tactical advantage. Technology and biosecurity have replaced land and labor as the deciding factors of market share. If you are betting on the future, look toward the nations investing in automated cold-chain logistics rather than just more barns. The sheer irony is that the more we industrialize, the more vulnerable the system becomes to a single biological breach. I believe that Brazil will eventually overtake the northern hemisphere due to their massive grain surplus and land availability. We are entering a decade of radical supply chain realignment where regional clusters will replace the global free-for-all. The crown is heavy, slippery, and currently heading south.