The shifting landscape of professional services and why the crown is heavy

The thing is, calling someone "number one" in this industry is a bit like calling a particular wave the biggest in the ocean; by the time you've measured it, the tide has already shifted. For decades, the hierarchy was somewhat static, but the digital revolution turned the Big 4 into tech companies that happen to do taxes. People don't think about this enough, yet the transformation from "bean counters" to "cloud architects" is exactly why the rankings are so volatile right now. Deloitte, PwC, EY, and KPMG aren't just competing with each other anymore—they are fighting McKinsey for strategy and Google for talent. It’s a messy, high-stakes brawl where audit quality and consulting prowess are the primary weapons of choice.

The evolution from Big 8 to the modern quartet

History matters here because the consolidation of these firms wasn't inevitable. We started with the Big 8, then the Big 6, and finally the Big 5 before Arthur Andersen’s spectacular, Enron-fueled implosion in 2002 left us with the current four pillars. This consolidation created unprecedented systemic importance—the "too big to fail" of the accounting world. But because these firms operate as networks of locally owned member firms rather than a single global corporation, the "number one" title is often a mathematical aggregation of thousands of smaller balances. It is a fragmented empire held together by a shared logo and a very expensive brand book.

Defining the metrics of dominance in a post-pandemic economy

How do we actually measure "best"? Revenue is the loudest metric, of course, but headcount and geographical footprint tell a different story about influence. If a firm has 450,000 employees but lower margins than a competitor with half that size, who is actually winning? Honestly, it’s unclear. Some partners argue that prestige and client satisfaction scores are the only metrics that don't lie, except that every firm claims to be the most trusted advisor in their own marketing glossies. The issue remains that a firm might be the leader in North America while barely cracking the top three in the Asia-Pacific region.

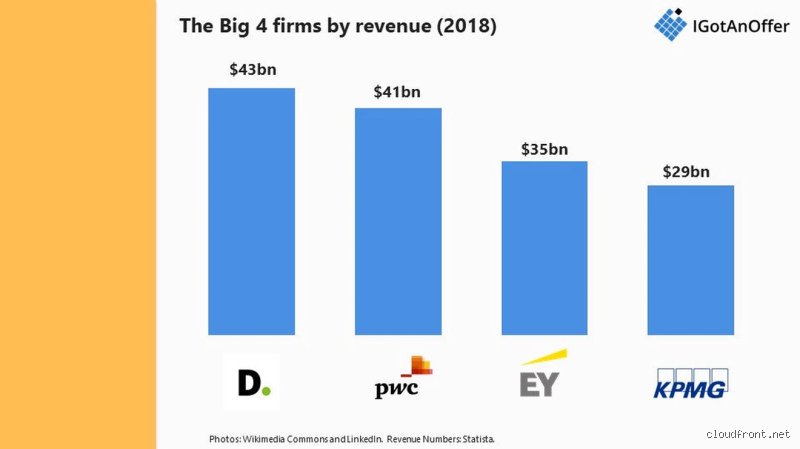

The Deloitte Juggernaut: Analyzing the revenue king’s strategy

Deloitte didn't just stumble into the top spot; they engineered it through a relentless expansion into multi-disciplinary services that many thought would be their undoing. Back in the early 2000s, when other firms were spinning off their consulting arms due to regulatory pressure (think EY selling to Capgemini or PwC’s arm going to IBM), Deloitte kept theirs. That decision changed everything. By maintaining a massive, integrated consulting practice, they were perfectly positioned to catch the wave of digital transformation that defined the last decade. And while the others had to rebuild from scratch, Deloitte was already sprinting.

The power of the multidisciplinary model

Critics often point to conflict of interest risks as the dark side of this "one-stop-shop" approach. But from a purely business perspective, having an auditor in the basement and a cybersecurity expert in the boardroom of the same client is a goldmine. Because Deloitte has such a massive footprint in Human Capital and Strategy, they can weather a downturn in M&A activity better than a firm that relies heavily on deal flow. It’s a diversified mutual fund of professional services. Which explains why their 2023 growth remained robust even as the global economy started to look a bit shaky around the edges.

Market share and the 14.9 percent growth leap

In the fiscal year ending May 31, 2023, Deloitte reported a 14.9% increase in revenue in local currency. That is a terrifying number for competitors. It’s not just growth; it’s an aggressive capture of market share during a period of global uncertainty. They are currently pulling in billions more than PwC, their closest rival, creating a buffer that hasn't been this wide in years. Does this make them the "best" to work for? Not necessarily, as the "Green Dot" culture is notoriously intense, often demanding a level of commitment that makes a 60-hour work week look like a part-time hobby. But in terms of sheer economic gravity, they are the sun around which the other three orbit.

PwC and the battle for the silver medal

PricewaterhouseCoopers—or PwC for those who prefer brevity—has traditionally been seen as the "gold standard" for audit. They have a formidable prestige that often allows them to charge a premium over their peers. Yet, they found themselves in the second spot, trailing Deloitte's revenue by several billion dollars. Why? Because while they are giants in Assurance and Tax, their consulting growth, though impressive, hasn't quite matched the sheer volume of Deloitte’s massive global machinery. But don't count them out; their "New Equation" strategy is a multi-billion dollar bet on Trust and Outcomes that aims to reclaim the throne by 2026.

The Australian tax leak scandal and brand resilience

Where it gets tricky for PwC is managing the fallout from localized disasters, like the 2023 tax leak scandal in Australia which saw the firm banned from certain government contracts and forced a massive internal restructuring. Such events prove that being "number one" is a precarious state of existence. One rogue partner in one corner of the globe can tarnish a brand that took a century to build. As a result: the firm has had to pivot hard toward ESG and AI-driven transparency to prove to regulators that they can still be the world's most trusted gatekeepers. It’s a classic case of a legacy giant trying to dance in a hurricane.

The chasing pack: Why EY and KPMG play a different game

EY (Ernst & Young) and KPMG are often lumped together as the "smaller" of the Big 4, but let’s be real: we are still talking about organizations with annual revenues exceeding $30 billion. They aren't small by any human standard. EY recently tried to pull off a daring maneuver called "Project Everest"—a plan to split their audit and consulting wings into two separate companies. I personally thought it was a brilliant, if risky, attempt to escape the regulatory shackles that prevent them from selling consulting services to audit clients. Except that it failed. The internal friction between audit partners and consulting partners became a civil war that eventually scuttled the deal, leaving EY to pick up the pieces of a visionary but ultimately aborted strategy.

KPMG’s niche dominance and the "Big 4" hierarchy

KPMG is consistently the fourth in the rankings, but they have carved out a specific identity as the most "local" of the global firms. They often dominate in middle-market services and have a surprisingly strong grip on the banking sector in various European and Asian markets. However, the gap between KPMG and Deloitte is now more than $30 billion. That’s not a gap; it’s a canyon. Does that matter to a client in Berlin looking for tax advice? Probably not. But in the global war for talent and technology investment, having a smaller war chest means you have to be twice as smart with every dollar you spend. Hence, their focus on strategic alliances with Microsoft and Google to bridge the tech gap without having to build everything in-house.

Shattering the Glass Myths: Common Misconceptions

The Revenue Equals Quality Fallacy

The problem is that you probably think the biggest balance sheet implies the sharpest audit. It does not. While Deloitte consistently towers over the others with its 2024 global revenue hitting $64.9 billion, size is often a byproduct of massive consulting acquisitions rather than pure technical superiority. We must distinguish between sheer mass and specialized precision. Because a firm dominates the Fortune 500 audit list, it does not mean their tax advisory team in a mid-sized regional hub is superior to a smaller rival. Aggregated financial data masks internal silos where performance fluctuates wildly. It is easy to assume the "No. 1" tag is a permanent badge of honor. Except that prestige is a local currency, spent and earned in specific city offices rather than at global headquarters.

The Uniformity Illusion

You might believe every office under the same brand umbrella operates with identical DNA. This is a mirage. The Big 4 are decentralized networks of independent member firms. If you hire PwC in London, your experience might share zero commonalities with a PwC engagement in Tokyo or Berlin. Each entity navigates its own regulatory environment and cultural nuances. This explains why one firm might lead in financial services in Manhattan while another dominates the energy sector in Houston. And let's be clear: Who is no. 1 in Big 4 depends entirely on which partner is signing your engagement letter. The logo on the coffee mug matters less than the specific human expertise in the room.

The Stealth Factor: Culture and The "Hidden" Exit Value

The Pedigree Paradox

Let's look at the "exit op" game, which remains the primary driver for high-tier talent entering these monoliths. While McKinsey or BCG often take the spotlight, the Big 4 alumni network is arguably the most powerful quiet force in global business. PwC often claims the top spot for "prestige" in various employee surveys, yet EY has aggressively branded itself as the most entrepreneurial of the pack. If you want to become a CFO, the audit-heavy background of KPMG might serve you better than a generalist consulting stint elsewhere. But here is the irony: the firm that works you the hardest often provides the most resilient resume (though your mental health might disagree). The issue remains that Who is no. 1 in Big 4 is a question of career trajectory, not just firm-wide profit margins. Which firm has the highest concentration of partners who actually mentor? That is the real metric, yet it stays buried under glossy brochures and corporate jargon.

Frequently Asked Questions

Which firm currently leads in global market share?

Deloitte remains the undisputed heavyweight champion in terms of total aggregate revenue, reporting nearly $65 billion for the 2024 fiscal year. They have successfully pivoted into a technology-first consultancy, which allows them to outpace the audit-focused growth of their peers. This massive lead is largely fueled by their staggering 14.9% growth in the Americas alone. Yet, when you strip away the consulting layers, the gap in core audit services between them and PwC is significantly narrower. As a result: the crown stays with Deloitte for now, but their dominance relies heavily on maintaining a lead in digital transformation projects rather than traditional accounting.

Does the brand name impact my future salary prospects?

Data suggests that the specific firm name on your CV creates a marginal difference in initial exit salary, usually fluctuating by only 5% to 8% between the top and bottom of the quartet. PwC and Deloitte frequently trade blows for the "most prestigious" title in Vault rankings, which can lead to slightly more aggressive poaching by private equity firms. The reality is that your specific industry specialization—such as ESG reporting or cybersecurity—dictates your market value more than the firm's global ranking. In short, the market cares that you survived the Big 4 environment, regardless of which specific skyscraper you occupied. Can a brand name really replace three years of grueling 80-hour work weeks? Not likely, but it certainly opens the door for the interview.

Who is the best choice for a mid-market company?

KPMG and Grant Thornton (though the latter is technically "Big 6") often compete fiercely for the mid-market space where agility is prized over sheer scale. KPMG has traditionally positioned itself as more accessible to non-enterprise clients, focusing on bespoke tax and advisory solutions that feel less like a factory line. While EY and Deloitte chase the multi-billion dollar tech giants, a mid-cap firm might find themselves ignored by the largest partners at those firms. Which explains why smaller organizations often find better value and senior-level attention at the firms ranked third or fourth by revenue. It is better to be a "big fish" client at a slightly smaller firm than a rounding error at the global leader.

A Final Verdict on Supremacy

Stop looking for a single name to sit on the throne because the throne is a modular piece of furniture. Deloitte wins the revenue race, PwC often captures the prestige crown, and EY frequently leads on innovation and workforce transformation. If we are being honest, the obsession with Who is no. 1 in Big 4 is a distraction from the reality of professional services. My position is firm: the best firm is the one that hasn't recently been hit by a massive independence scandal in your specific jurisdiction. We must accept that these entities are too large to be "best" at everything simultaneously. You should choose based on the sector-specific rankings and the local office's reputation rather than a global marketing budget. The numbers tell a story of growth, but the culture tells the story of your daily life.