The Illusion of the Seventy-Grand Milestone: Breaking Down the Numbers

For decades, hitting this specific five-figure mark felt like arriving. You made it. Except that inflation recently took a sledgehammer to that milestone, leaving many middle-class workers wondering why their bank accounts still feel so remarkably fragile at the end of the month.

The Statistical Reality of Median Earnings

Let us look at the hard data without the emotional baggage. The U.S. Census Bureau recently pegged the median household income at roughly $75,000, which means pulling in seventy grand as an individual actually places you in a pretty solid position compared to the broader population. But the thing is, households often rely on two pools of money. When you are flying solo, that single income stream has to shoulder every single economic shock alone. I look at these metrics daily, and frankly, comparing an individual paycheck to household data is a trap that leads to massive financial frustration.

What Happens to Your Check Before It Hits the Bank?

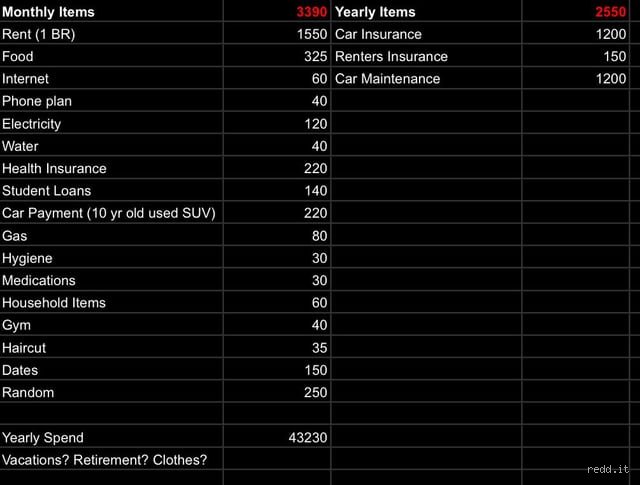

Gross pay is a fantasy. If you sign an employment contract in a state like Ohio or Georgia, that top-line number looks great until Uncle Sam and your local treasurer take their mandatory cuts. After federal income taxes, FICA, state levies, and perhaps a modest 4% 401(k) contribution—because skipping retirement savings is economic suicide—your take-home pay shrinks fast. You are looking at roughly $4,200 to $4,500 a month in actual, usable cash. And that changes everything.

The Geography of Affordability: Why Location Alters Your Financial Reality

This is where it gets tricky. A salary of seventy thousand dollars does not possess a fixed value; its utility behaves like a chameleon depending on your exact coordinates on a map.

The Urban Tax: Survival in High-Cost-of-Living Areas

Try making is $70,000 a year a lot of money sound convincing to a software junior paying rent in Manhattan or San Francisco. In Brooklyn, the average monthly rent for a one-bedroom apartment routinely clears $3,500—consuming almost your entire net monthly income before you even buy a single gallon of milk or pay an electric bill. It is mathematically impossible to live alone there on this budget without sinking into credit card debt. Thus, in these coastal metros, this wage actually borders on the working-poor spectrum, forcing professionals into multi-roommate apartments well into their thirties.

The Heartland Advantage: Scoring Room to Breathe

But move that exact same paycheck to Indianapolis, San Antonio, or Akron, Ohio? Suddenly, the narrative flips completely. In those markets, a clean, modern one-bedroom apartment might only set you back $1,100 a month, which complies beautifully with the traditional 28% housing rule. You can buy groceries at Kroger without checking your banking app in a panic at the register. You might even save enough for a down payment on a house within three years. Yet, experts disagree on whether these cheaper markets will stay affordable for long, given the massive influx of remote workers shifting local real estate dynamics.

The Hidden Cash Eaters That Kill a Respectable Wage

We need to talk about the structural obligations that the typical personal finance guru loves to ignore when drawing up hypothetical budgets.

The Millennial and Gen Z Tax: Student Loans and Transportation

Imagine graduating from the University of Missouri with the average undergraduate debt load of $30,000. That is a monthly bill of roughly $350 under standard repayment terms. Add a modest car payment—since public transit is a myth in most of America—because the average used car now costs an absurd amount of money, and you are bleeding another $500 monthly for a depreciating asset. Is $70,000 a year a lot of money if nearly a thousand dollars vanishes every month just to cover the cost of getting to your job and paying for the degree that secured it?

The Healthcare Wildcard

People don't think about this enough until they find themselves sitting in an urgent care lobby on a Tuesday morning. High-deductible health plans can mean paying $5,000 out of pocket before your insurance coverage kicks in for anything substantial. A single bad fracture or an emergency appendectomy can completely wipe out an entire year of diligent saving on a seventy-thousand-dollar income. Hence, financial stability on this salary is often just an illusion that persists only as long as you remain perfectly healthy.

How k Compares to Alternative Livelihoods and Lifestyles

To truly understand where this income bracket sits, we have to contrast it against the extremes of the modern American workforce.

The Shift from Minimum Wage to the Middle Class

Perspective matters immensely here. To a worker earning the federal minimum wage of $7.25 an hour—or even a more progressive state minimum of $15 an hour—an income of seventy grand feels like absolute opulence, representing a world where you do not have to choose between keeping the lights on or buying prescription medication. It represents freedom from the daily, grinding anxiety of basic survival. As a result: the psychological relief of hitting this tier is undeniable if you have spent years scraping by on hourly shifts.

The Gap Between Middle Management and the True Wealth Elite

But let’s not get delusional about our economic status. This salary keeps you firmly entrenched in the working middle class; you still exchange your time directly for dollars, and if you stop working, the money stops flowing. You cannot afford luxury vehicles, impromptu trips to Europe, or unvetted investment properties. In short, it provides comfort, but it provides zero systemic leverage.

Common mistakes and dangerous misconceptions

The gross income optical illusion

Let's be clear: seventy grand is a phantom number. People look at a job offer and instantly calculate their lifestyle based on the sticker price. They forget that Uncle Sam always takes his cut first. After federal income taxes, FICA, and state levies, that shiny salary shrinks dramatically. If you live in a high-tax state like California or New York, your take-home pay might plummet to roughly

$52,000 annually. That leaves you with about $4,330 a month. Suddenly, the math changes. You aren't budgeting with seventy thousand; you are surviving on significantly less.

The lifestyle creep trap

Earning more usually triggers spending more. It is a psychological reflex. When people cross the threshold into middle-class comfort, they trade used sedans for financed SUVs. They swap home-brewed drip coffee for artisanal lattes. The problem is that small upgrades aggregate into massive fixed expenses. You feel rich, so you act rich. Yet, your savings account remains bone dry. Studies show that nearly

40% of high earners living in urban centers save less than 5% of their paycheck. They are trapped on a hedonistic treadmill, running faster just to stay in the exact same financial place.

Ignoring the local reality

A salary is only as powerful as the zip code where it is deposited. Believing that a fixed income carries the same weight everywhere is a catastrophic mistake. In Wichita, Kansas, this wage buys a sprawling four-bedroom house and a comfortable life. In San Francisco, it makes you eligible for low-income housing programs. Geographic economic disparity is real. You cannot evaluate whether

is $70,000 a year a lot of money without mapping your local cost of living index.

---

The stealth tax on single earners

The solo living penalty

Everyone talks about inflation, but we rarely analyze the brutal economic math of being single. Society rewards couples. When two people earn a combined middle-class wage, they split rent, utilities, and subscription services. They optimize tax brackets. For a solo professional, however, the financial burden is absolute. You pay 100% of the rent for your one-bedroom apartment. There is no one to divide the internet bill with.

As a result: your seventy-thousand-dollar purchasing power is effectively slashed by thirty percent compared to a dual-income household. This hidden penalty prevents single folks from building wealth at the same velocity. Want to buy a home? You need a massive down payment generated entirely by your own sweat. It is an uphill battle. (And let's not even start on the skyrocketing cost of individual health insurance premiums). Expert wealth management requires acknowledging this systemic disadvantage. To combat it, solo earners must aggressively automate their investments early, treating savings as a non-negotiable expense rather than an afterthought.

---

Frequently Asked Questions

Is ,000 a year a lot of money for a family of four?

No, it is generally considered tight for a household of that size. The federal poverty level for a family of four sits near $31,000, but realistic data from the Economic Policy Institute shows that a family needs closer to

$85,000 annually to secure true economic stability in most American metro areas. Childcare costs alone can easily consume $15,000 per child annually, which obliterates a middle-management paycheck. Food inflation and family health insurance plans further erode your purchasing power. While you will certainly survive, you will likely live paycheck to paycheck without much room for family vacations or robust college savings accounts.

Can you buy a house comfortably with this specific salary?

Yes, but your geographic location and existing debt profile will entirely dictate the reality of that transaction. Mortgage lenders typically utilize the 28/36 rule, meaning your housing costs shouldn't exceed 28% of your gross monthly income. With a $70k income, your maximum monthly housing payment should hover around $1,630. Given modern interest rates, this limits your maximum loan amount to roughly

$210,000 to $240,000 assuming a standard down payment. In the Midwest or Rust Belt, that budget buys a beautiful, move-in-ready property. Conversely, if you are shopping in Boston or Seattle, that amount won't even buy a dilapidated studio condo.

How does this income compare to the national median wage?

It tracks significantly higher than what the average individual worker takes home. Recent data from the U.S. Bureau of Labor Statistics indicates the median individual earnings hover around

$59,000 per year for full-time employees. This places you comfortably above the halfway mark nationwide. Which explains why many people view this specific wage as a major career milestone. You are out-earning a massive percentage of the population. But does that make you wealthy? Absolutely not, because macroeconomic factors like nationwide housing shortages have decoupled median wages from historical purchasing power.

---

The final verdict on the seventy-thousand milestone

Stop looking at national averages to validate your financial status. The reality is that seventy thousand dollars is no longer the golden ticket to the effortless American Dream. It is a solid, working-class baseline that demands strict discipline and zero illusions. If you are single in an affordable mid-sized city, celebrate because you can live exceptionally well while funding a vibrant retirement portfolio. But if you are raising a family or trying to conquer a coastal metropolis on this lone salary, you will face a constant, grinding psychological pressure. Wealth isn't a static number on a W-2 form. True financial freedom is determined entirely by the gap between what you bring in and what the local economy forces you to shell out.