Decoding the Schedule K-1: Why the IRS Views This Revenue Differently

The core of the problem lies in how Washington defines a dollar made from sweat versus a dollar made from capital. When you receive a Schedule K-1 (Form 1065) or a Form 1120-S, you are looking at pass-through tax reporting, meaning the entity itself pays no corporate income tax. Instead, profits flow straight to your personal return. But here is where people don't think about this enough: pass-through mechanics do not automatically transmute corporate profits into what the federal government considers "earned" compensation.

The Anatomy of Form 1065 and Form 1120-S

Look at your paperwork. If your cash is coming from an S-Corporation via Form 1120-S, Box 1 reports ordinary business income. That specific number is almost never earned income. Why? Because the tax code assumes an S-Corp owner extracts their "earned" portion via a traditional W-2 salary, complete with FICA tax withholdings. On the flip side, a partnership filing Form 1065 handles things through a completely different lens, which explains why general partners often see their net earnings from self-employment listed explicitly in Box 14. That little box changes everything.

The Legal Line Between Active Labor and Passive Capital

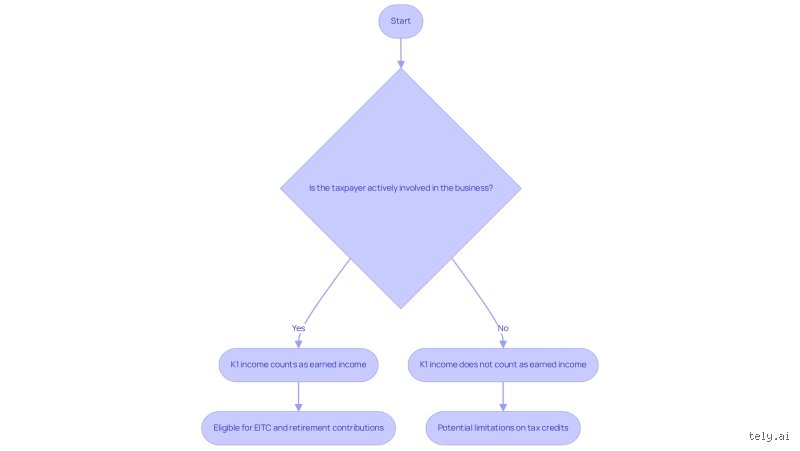

I have analyzed hundreds of portfolio structures, and the consensus among seasoned practitioners is clear: the IRS hates when taxpayers try to have it both ways. To qualify as earned revenue, money must derive from physical or mental labor. If you merely cut a check in 2024 to fund a trendy Brooklyn coffee shop but never stepped behind the counter, that resultant K-1 distribution is pure passive income. Yet, if you are the operator managing day-to-day logistics? The distinction blurs, except that the IRS has codified strict material participation standards under Section 469 to prevent people from arbitrarily reclassifying their investment yields when it suits them.

When K-1 Income Transforms into Earned Revenue: The Self-Employment Tax Gateway

The absolute litmus test for whether your K-1 distributions can fund a retirement account or qualify you for specific tax credits is the presence of Self-Employment Contributions Act (SECA) taxes. If your net distribution is subject to that hefty 15.3% self-employment tax rate, congratulations: you have earned income. If it bypasses that tax, it is classified as investment or passive flow, which means you cannot use it to justify a maximum contribution to a Roth IRA.

The Box 14 Crux on Partnership Returns

Let us talk numbers. When a general partnership passes profits to its partners, those individuals must look directly at Box 14, Code A of their Schedule K-1. If there is a $45,000 entry there, that specific amount represents your net earnings from self-employment. That is your magic ticket. That sum can be used to calculate your maximum deductible contribution to a Solo 401(k) or a SEP-IRA. But if you are a limited partner in an Ohio real estate syndication, Box 14 will likely sit blank, while Box 2 reflects passive rental real estate income. Do you see the difference? The issue remains that one person’s active livelihood is another person’s hands-off portfolio yield.

The S-Corp Loophole and the Reasonable Compensation Trap

S-Corporations offer a fascinating, albeit dangerous, workaround. Business owners frequently utilize S-Corps specifically to avoid self-employment taxes on their ordinary business income. Imagine your Austin-based software consultancy generates $200,000 in net profit. If you take a W-2 salary of $80,000, that specific portion is undisputedly earned income. The remaining $120,000 flows through to your K-1 as ordinary income from an S-Corp. Is that remainder earned? Absolutely not. It escapes the 15.3% SECA tax, which is fantastic for your current cash flow, but it cannot be used to boost your retirement contribution room. It is a calculated trade-off that many entrepreneurs misunderstand until their CPA drops the bad news in April.

The Hidden Impact on Retirement Accounts and Government Subsidies

Where it gets tricky is when small business owners attempt to leverage their business success to qualify for federal programs or wealth-building vehicles. The government uses different definitions of income for different benefits, which creates an absolute minefield for the uninitiated.

Why Your Roth IRA Care About Box 14

To contribute to a Roth IRA in 2026, you need what the IRS calls "taxable compensation." If a sole proprietor or a general partner wants to maximize their $7,000 annual contribution limit (or $8,000 if they are over age 50), they must ensure their Box 14 earnings support that amount. You cannot fund a retirement account using passive dividends or S-Corp K-1 distributions. What happens if you do? You face a brutal 6% excess contribution penalty every single year the mistake remains uncorrected in your account. Honestly, it's unclear why the software platforms don't flag this more aggressively, given how often modern gig-economy workers fall into this exact trap.

The Earned Income Tax Credit (EITC) Disconnect

Consider the plight of a startup founder who pours 80 hours a week into an LLC but takes minimal salary to preserve runway. Their K-1 might show a modest profit, but if that profit is not flagged as self-employment income, they cannot claim the EITC, an incredibly valuable credit worth up to several thousand dollars for families. For instance, in a well-documented 2022 tax court case involving an active LLC member in Chicago, the taxpayer argued that their sheer physical presence at a manufacturing facility should naturally qualify their K-1 distributions as earned income for credit purposes. The court disagreed completely. The legal reality is rigid: no self-employment tax paid means no earned income recognized for the credit, period.

Comparing K-1 Types: How Entity Choice Dictates Your Tax Status

To fully grasp how your specific income will be treated, we need to stack the different business structures side by side. It becomes obvious quite quickly that the entity wrapper you choose dictates your tax reality far more than the actual work you perform.

The Multi-Member LLC vs. The Limited Partnership

In a standard Multi-Member LLC, members who actively manage the business are treated essentially like general partners, hence their K-1 income is usually hit with self-employment taxes. Contrast this with a formal Limited Partnership structured under state law. In that scenario, the limited partners are legally barred from active management; their liability is limited, and as a direct result, their K-1 income is statutorily excluded from self-employment tax under Internal Revenue Code Section 1402(a)(13). They are completely different beasts, even if both operations are making identical net profits in the same sector.

The financial ramifications of these structural nuances are stark when examined across different business entities:

Look closely at that matrix. It exposes the fallacy of the blanket statement "I own a business, so all my revenue is earned." If you are running an S-Corp, your K-1 ordinary income is dead space for retirement calculations. If you are an active LLC operator, that same dollar amount is live ammunition for your financial planning. Experts disagree on whether the IRS will eventually close the S-Corp loophole regarding reasonable compensation and distributions, but for now, the data shows a clear divergence in how these entities are policed. The conversation naturally moves from defining this income to optimizing it, which requires understanding how guaranteed payments alter the landscape entirely.

Common Misconceptions Blocking Your Tax Strategy

The "Passive vs. Active" Mirror Trick

Many business owners assume that if they sweat for their company, every dollar distributed to them magically qualifies as earned income. The problem is, the Internal Revenue Code does not care about your sweat equity; it cares about structural definitions. You might clock eighty hours a week running an S-corporation, yet your distributive share on Schedule K-1 remains non-earned revenue. Why? Because the IRS views that specific bucket as a return on capital investment rather than a direct payment for your services. It feels deeply unfair, yet the tax code operates on cold legal forms, not your physical exhaustion.

Conflating Gross Receipts with Net Self-Employment Profits

Another frequent trap involves staring at Box 1 of a Partnership K-1 and assuming that entire figure builds your retirement contribution room. Let's be clear: gross distributions differ entirely from the net numbers calculated on Schedule SE. If your partnership incurred massive Section 179 depreciation deductions, your actual net earnings from self-employment could shrink to zero. Does K1 income count as earned income under these circumstances? Absolutely not, because your net bottom line dictates the final outcome, leaving you with zero room for SEP-IRA contributions despite healthy cash distributions during the fiscal year.

The S-Corporation Salary Illusion

S-corporation shareholders frequently stumble here. They look at their total K-1 payout, bypassing the W-2 requirement entirely. If you fail to pay yourself a reasonable salary via a W-2, your K-1 distributions cannot step in to act as a substitute for earned revenue. The issue remains that the IRS explicitly mandates a distinction between corporate wages and ownership distributions, penalizing those who try to blend the two together.

Advanced Strategic Playbook for High-Net-Worth Partners

The Limited Partner Material Participation Pivot

Can a limited partner ever break through the structural barrier to claim earned revenue? The answer relies heavily on the net earnings from self-employment classification, which usually excludes limited partners under Section 1402(a)(13). Except that, if you provide guaranteed payments for services rendered to the partnership, that specific slice transforms into earned compensation. This creates a powerful planning lever. By structuring your partnership agreement to guarantee payments for specific operational oversight, you deliberately trigger the self-employment tax. Why would anyone want to pay more tax? Because doing so creates the necessary legal foundation to fund a defined benefit pension plan, allowing you to shield up to $275,000 of total annual revenue from immediate federal taxation.

Frequently Asked Questions

Does K1 income count as earned income for traditional or Roth IRA contribution purposes?

No, it generally does not, unless it explicitly appears in Box 14 of a Form 1065 marked as self-employment earnings. For instance, an S-corporation K-1 showing $150,000 in Box 1 ordinary business income provides exactly $0 of qualifying compensation for IRA purposes. You must rely entirely on your Box 1 W-2 wages from that corporate entity to satisfy the statutory limits, which top out at $7,000, or $8,000 if you are age fifty or older. Attempting to fund a Roth IRA using unearned partnership distributions triggers a 6% excess contribution penalty every single year the mistake remains uncorrected. As a result: reliance on the wrong K-1 box can trigger a cascading audit that strips away your targeted retirement growth advantages.

Can I use my S-corp K-1 business distributions to claim the Earned Income Tax Credit?

The Earned Income Tax Credit demands specific, statutorily defined compensation, meaning ordinary business income from an S-corporation K-1 fails the compliance test completely. The IRS demands to see W-2 wages or true statutory self-employment profit before they authorize this specific credit, which can max out around $7,430 for families with three or more qualifying children. If your entire livelihood flows through an S-corp K-1 without a corresponding W-2, your qualifying income for this credit reads as mathematically non-existent. But wouldn't it make sense to evaluate the global tax picture before rewriting your corporate payroll structure? In short, maximizing this credit through wages might inadvertently increase your payroll tax liability by 15.3%, wiping out the credit's financial benefit entirely.

How do guaranteed payments on a partnership K-1 alter my self-employment tax obligations?

Guaranteed payments listed in Box 4 of Form 1065 represent the holy grail for individuals searching for earned compensation from business entities. These payments bypass the general rule excluding limited partners, flowing directly onto Schedule SE to face the standard 15.3% self-employment tax rate. For example, a partner receiving a $50,000 guaranteed payment possesses $50,000 of true earned revenue, irrespective of whether the partnership itself records a net loss for the year. This specific mechanism serves as the primary gateway for partners to legitimize their retirement plan contributions and build social security credits. Which explains why savvy tax professionals aggressively utilize guaranteed payment structures to manipulate the exact ratio between passive distributions and active, taxable compensation.

The Definitive Verdict on K-1 Revenue Classification

The obsessive quest to transform passive business distributions into earned compensation reveals a deeper structural conflict within modern asset protection and tax reduction planning. We must stop treating Form K-1 as a monolithic tax document because doing so ignores the profound legal chasms separating limited partnerships, general partnerships, and S-corporations. My firm position is that business owners routinely jeopardize their retirement safety by misclassifying this revenue, blinded by the mere fact that they work hard for their money. The law is entirely indifferent to your effort; it yields only to precise entity structuring and meticulous box checked alignment. Relying blindly on your ordinary business distributions to fund wealth-building vehicles without validating Box 14 or W-2 cross-references is an act of fiscal recklessness. You cannot simply wish your passive distribution into active compensation (though thousands of audited entrepreneurs try every year). True financial mastery requires acknowledging that your K-1 is a dual-natured beast, requiring deliberate engineering to serve your broader wealth preservation goals safely.